What PE Operating Partners Actually Want From a Portfolio Company’s CMO

- Roger M.

- Mar 24

- 5 min read

Updated: 5 days ago

The operating partner sits across the table at the quarterly board meeting. The CMO has prepared 14 slides. Impressions are up. Social engagement is growing. The brand refresh is on track. The website redesign launches next month.

The operating partner asks one question: what did marketing contribute to ARR this quarter?

The room goes quiet. Not because the CMO lacks talent — but because they have never been asked to answer marketing questions in the language of a value creation plan. They were hired to run campaigns. The operating partner needs someone who runs a revenue engine.

This disconnect repeats across portfolio company after portfolio company. It is not a personality clash. It is a structural misalignment between what CMOs are trained to deliver and what PE ownership demands. Understanding the gap — and knowing how to close it — is the difference between a marketing function that creates enterprise value and one that quietly burns cash until exit.

The structural shift: why marketing is now the primary value creation lever

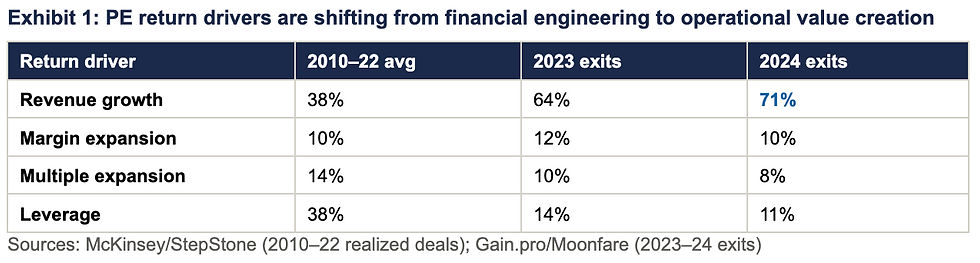

Between 2010 and 2022, leverage and multiple expansion carried 59 percent of buyout returns. Revenue growth and EBITDA margin expansion — the operational levers — contributed the remaining 41 percent. But those tailwinds have faded structurally. Debt as a percentage of entry multiples declined from 44 percent in 2016 to 37 percent in 2025. Entry multiples reached a record 11.8x EBITDA. For deals above $500 million, the median hit 18.1x.

Revenue growth now accounts for 71 percent of value creation in 2024 PE exits (Gain.pro/Moonfare 2026), up from 64 percent in 2023. Buyout fund IRRs averaged just 5.7 percent on a pooled basis between 2022 and 2025 — the lowest sustained period since the early 2000s.

The marketing function sits at the centre of this shift. It is responsible for pipeline generation, demand creation, and conversion infrastructure — the inputs that drive the revenue growth now constituting the majority of PE returns. Yet most portfolio company CMOs were not hired with this context.

What does a PE firm look for in a portfolio company CMO?

Operating partners evaluate marketing leadership against five non-negotiable requirements.

1. Financial fluency over creative vision

The first requirement is financial literacy. An operating partner needs a CMO who can construct a board deck the investment committee would find credible — ARR waterfall analysis, CAC payback period by channel, pipeline coverage ratios (the 3x minimum most operating partners treat as table stakes), and EBITDA contribution modelling.

McKinsey’s 2026 survey of 300 global LPs found that 53 percent ranked a GP’s value creation strategy among their top five criteria for manager selection — third behind performance and team quality. When the LP asks how marketing drives value, the GP needs financial metrics tied to enterprise value. The CMO who cannot produce them is invisible in the one conversation that matters most.

2. Attribution that proves causation

Operating partners want multi-touch attribution configured in the CRM with consistent UTM tagging and closed-loop reporting that traces every deal to its originating source. The foundational work — clean CRM data, lifecycle stage definitions, proper source tracking — is what most portfolio companies lack. Operating partners want this built in the first 30 days.

3. A repeatable GTM that does not depend on the founder

McKinsey reports that 60 to 70 percent of PE-backed companies experience a C-suite change during ownership. If the GTM depends on one person’s relationships or personal brand, acquirers treat it as concentration risk and discount the valuation. Operating partners want a CMO who documents the ICP forensically, codifies the messaging playbook, and maps the relationship infrastructure so it belongs to the company.

4. Speed to impact

Value creation in PE is typically back-loaded — 6 percent of ending EBITDA margin generated in the final year, roughly 1 percent each prior year (McKinsey 2026). The best operators reverse this with a 100-day sprint: audit by day 30, GTM alignment by day 60, board-ready attribution by day 100.

5. Exit readiness from day one

The median company completing an IPO in 2025 is 13.5 years old with $218 million in revenue (Partners Capital). Acquirers scrutinise five dimensions: CAC defensibility, GTM repeatability, attribution cleanliness, customer concentration risk, and brand premium justification. Most companies fail on at least three.

How should a CMO report to PE investors?

Monthly operating reviews: Pipeline created and converted, marketing-sourced ARR (absolute and percentage of new logo revenue), CAC by channel with trend lines, conversion rates by funnel stage.

Quarterly board presentations: Progress against value creation plan milestones, ICP segment performance, competitive shifts, forward pipeline forecast — in the same format the operating partner uses across the portfolio.

Annual value creation reviews: Marketing’s explicit contribution to enterprise value — attributed revenue growth, efficiency-driven margin improvements, and exit readiness scores.

The through-line: marketing reports in the language of finance. Pipeline coverage, not lead volume. ARR contribution, not campaign impressions. CAC payback trajectory, not cost per click.

What KPIs matter to PE operating partners in marketing?

Operating partners focus on five KPIs that connect directly to enterprise value. Everything else is noise.

How does a fractional CMO support a value creation plan?

Most PE-backed companies at $10M–$50M ARR need strategic marketing leadership but cannot justify a full-time CMO at $236,000–$438,000 per year — not at their stage, and not when the risk of a mis-hire is compounded by the 60–70 percent C-suite turnover rate McKinsey documents.

A fractional CMO embeds at 15–25 hours per month. Attribution infrastructure in month one. GTM aligned to the value creation plan in month two. First board-ready report with marketing-sourced ARR data in month three. No equity dilution. No severance risk. No six-month ramp.

The exit backlog reinforces the urgency. Over 16,000 companies globally have been held more than four years — 52 percent of total buyout inventory. With Intelligence counts over 9,000 active portfolio companies in North America alone, 63 percent held more than four years. Apollo’s 2026 outlook describes a widening DPI gap creating “compelled sellers” — GPs under increasing pressure to crystallise value. Companies with clean, attribution-documented, repeatable GTM engines will command premium multiples. Those without will face valuation discounts.

For PE-backed companies that cannot yet afford a full-time CMO but can no longer afford to operate without one, the fractional model is not a compromise. It is the operating partner’s preferred solution.

Sources: McKinsey & Company, Global Private Markets Report 2026; Partners Capital, Insights 2026; Apollo Global Management, PE Opportunities 2026; Wellington Management, VC Outlook 2026; With Intelligence, PE Outlook 2026; Moonfare PE Outlook 2026 citing Gain.pro; Bain & Company Commercial Excellence Benchmark; StepStone Group SPI analysis; Glassdoor CMO Salary Data (Feb 2026).

Comments